Imagine earning $60,000 a year. You claim $15,000 in deductions, so the IRS taxes only $45,000. That simple step can save you hundreds or even thousands, depending on your bracket.

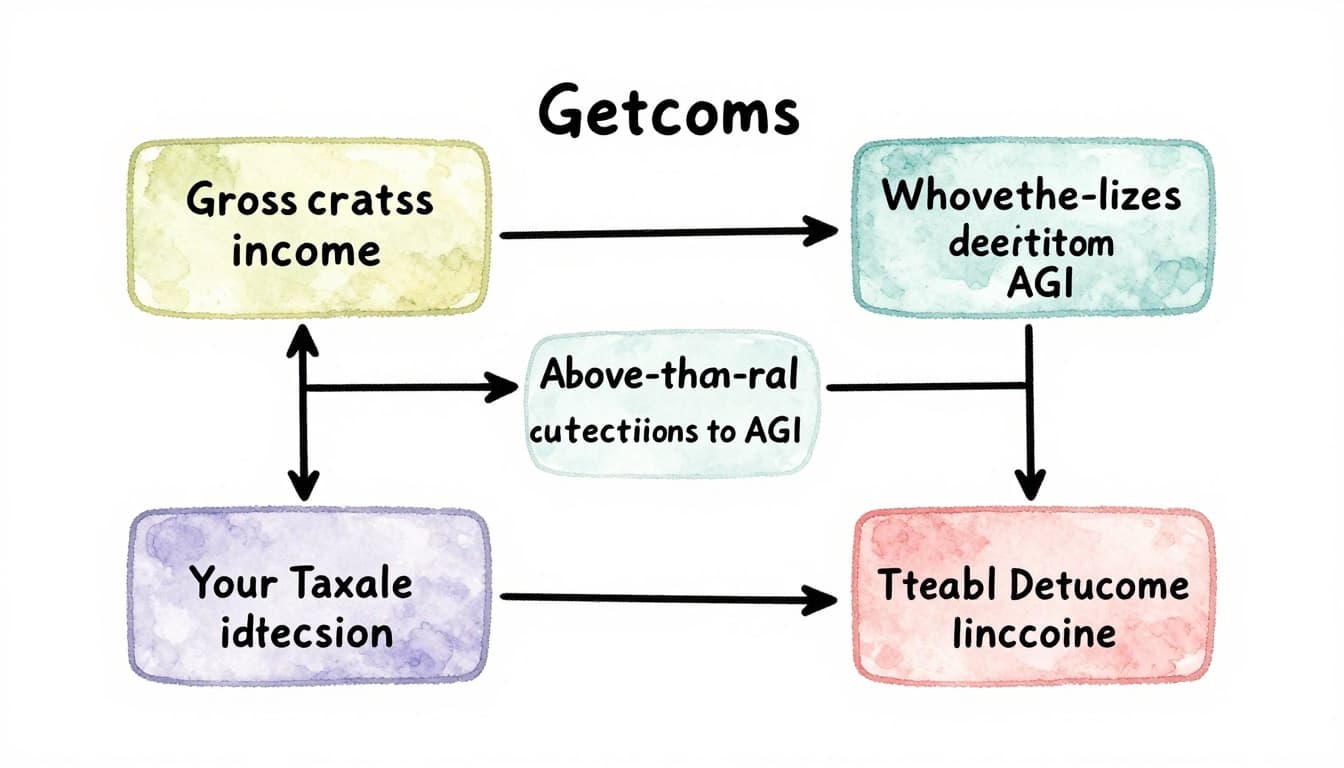

Deductions reduce your taxable income by subtracting eligible expenses from your gross pay. Start with total income, pull out above-the-line perks first to reach adjusted gross income (AGI). Then choose the standard deduction or itemize to get your final taxable amount. Lower that number, and your tax bill drops right away.

For 2025 taxes (filed in 2026), exciting updates make this easier. The state and local tax (SALT) cap jumps to $40,000, up from $10,000. New above-the-line breaks cover qualified tips up to $25,000 and overtime pay up to $12,500 if single or $25,000 joint. Standard deductions rise too: $15,750 single, $31,500 married filing jointly, $23,625 head of household. Seniors 65+ snag a $6,000 bonus on top.

Most folks take the standard route because it’s quick. Itemizing pays off if you live in a high-tax state or give big to charity. Above-the-line options work either way, so stack them for max savings.

We’ll break down standard versus itemized next. By the end, you’ll know exactly how to cut your taxable income and keep more cash.

Your Taxable Income Breakdown: Where Deductions Fit In

Your taxable income starts with gross income from wages, investments, and other sources. You subtract above-the-line deductions first. That gives you adjusted gross income, or AGI. Next, subtract either the standard deduction or itemized deductions. The result is your taxable income. The IRS applies tax rates to that final number.

Here is the simple process:

- Add up total income.

- Subtract above-the-line deductions to reach AGI.

- Subtract standard or itemized deductions.

- Tax your remaining taxable income.

For example, you earn $50,000. After $5,000 in above-the-line deductions, your AGI is $45,000. You take a $15,750 standard deduction. Taxable income drops to $29,250. In the 12% bracket, that saves you $1,890 compared to no deductions.

Deductions lower the income you tax. Credits, however, cut your tax bill dollar for dollar. Deductions save more in higher brackets. A $1,000 deduction at 37% saves $370. The same credit saves the full $1,000. Always stack above-the-line options first. They lower AGI and boost other breaks.

Standard Deduction: The Easy No-Receipts-Needed Option

Most people, about 87%, pick the standard deduction. It requires no receipts or records. Just claim the flat amount. These figures rose from 2024 due to inflation.

Here are the 2025 base amounts:

| Filing Status | Base Amount |

|---|---|

| Single or Married Filing Separately | $15,750 |

| Married Filing Jointly | $31,500 |

| Head of Household | $23,625 |

Add extra if you or your spouse are 65 or older: $2,000 for single or head of household, $1,600 per qualifying spouse if joint. A new senior bonus adds $6,000 for those 65+ (with AGI limits). For instance, a single filer 65+ gets $15,750 base plus $2,000 plus $6,000, for $23,750 total.

Take the standard if your itemized total stays below it. Tax software like TurboTax runs both options fast. Check IRS Publication 554 for seniors. A single filer with $60,000 AGI saves taxes on the full $15,750. That cuts 12% bracket taxes by about $1,890.

Itemized Deductions: Track Expenses for Bigger Wins

Itemize only if your totals beat the standard. List them on Schedule A. You need receipts for proof.

Key 2025 updates help. The SALT cap hits $40,000, up big from $10,000. It phases down above $500,000 AGI for singles. Deduct mortgage interest on up to $750,000 debt. Medical expenses count over 7.5% of AGI. Charitable gifts go up to 60% of AGI.

Compare options with this table for a single filer:

| Option | Amount Example |

|---|---|

| Standard | $15,750 |

| SALT | Up to $40,000 |

| Mortgage Interest | Varies, say $10,000 |

| Medical | Over 7.5% AGI |

| Charity | Up to 60% AGI |

| Total Itemized | Could top $30,000 |

Bundle donations in one year. Prepay property taxes before December 31. High-tax state residents often win big. See details on the SALT cap changes. Run numbers both ways for your best savings.

Above-the-Line Deductions: Claim These No Matter What

Above-the-line deductions lower your adjusted gross income right away. You claim them on Schedule 1 of Form 1040. Best part? They work whether you take the standard deduction or itemize. Everyone qualifies if you meet the rules. Stack a few, and your AGI drops fast. That opens doors to more tax breaks too. Let’s look at top ones that save real money.

Student Loans and Business Costs That Cut AGI Fast

Student loan interest stays a solid pick. You deduct up to $2,500 each year. However, it phases out if your modified AGI hits $80,000 to $95,000 for singles or $165,000 to $195,000 for joint filers. Check your loan statements. Paid interest? Enter it on line 21 of Schedule 1. A recent grad with $60,000 AGI claims the full amount. That saves about $300 in the 12% bracket.

Self-employed folks score big on business costs. Report them on Schedule C, then carry to Schedule 1. Track mileage at 70 cents per mile in 2025. Drove 5,000 business miles? Deduct $3,500. Home office counts too. Use the simple method at $5 per square foot, up to 300 square feet for a $1,500 max. Supplies like paper or software add up quick.

Gig workers and freelancers love these. Apps like QuickBooks or MileIQ make tracking easy. Here’s what fits best:

- Mileage: Log trips with an app; deduct 70 cents per business mile.

- Home office: Measure your space; claim $5 per foot if exclusive use.

- Supplies: Pens, internet, phone bills tied to work.

- Student loans: Combine with business if you freelance while paying debt.

One driver saved $4,000 last year. Start a log today. Your AGI falls, taxes follow.

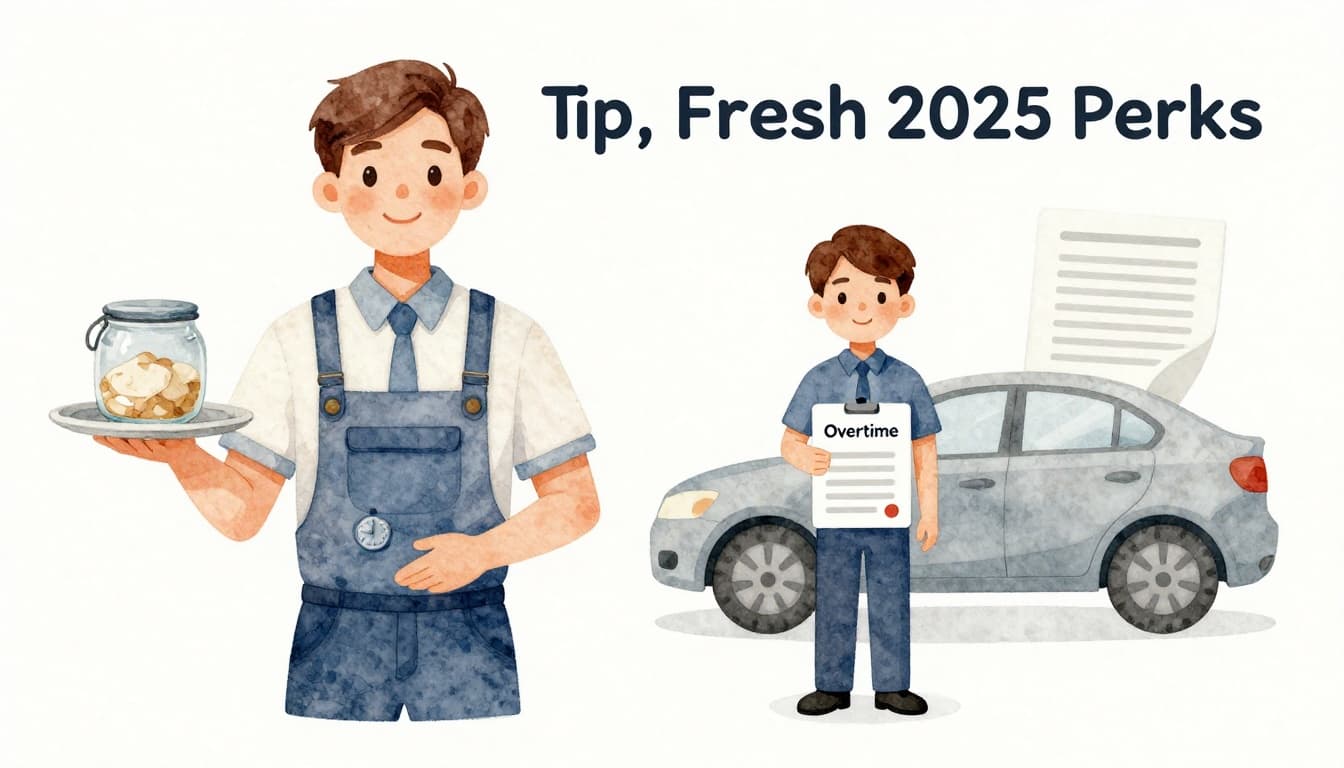

Fresh 2025 Perks: Tips, Overtime, and Car Loans

The One Big Beautiful Bill added fresh above-the-line wins for 2025. Claim them on new Schedule 1-A. Tips lead the pack for service workers. Deduct up to $25,000 in qualified tips from your W-2 or 1099. Phaseout starts at $150,000 MAGI for singles or $300,000 joint. A server earning $40,000 in tips drops AGI by the full amount. Savings hit $3,000 in taxes.

Overtime pay gets a boost too. Deduct up to $12,500 if single or $25,000 joint on premium overtime. Same phaseouts apply. Factory workers punch the clock extra? Claim the half-time portion. One hourly employee saved $1,500 after a busy year.

Auto loan interest shines for new rides. Deduct up to $10,000 on U.S.-assembled vehicles. Phaseout kicks in above $100,000 single or $200,000 joint. See TurboTax rules for OBBB car loan interest. Keep lender statements.

These perks help millions. Track pay stubs and loans now. Examples show big wins:

| Deduction | Max Amount (Single) | Phaseout Start | Example Savings (12% Bracket) |

|---|---|---|---|

| Tips | $25,000 | $150,000 MAGI | $3,000 |

| Overtime | $12,500 | $150,000 MAGI | $1,500 |

| Auto Loan | $10,000 | $100,000 MAGI | $1,200 |

File with software to catch them all. You keep more cash.

Real-Life Examples: See Deductions Slash Your Tax Bill

Real people just like you slash their taxes every year with deductions. These scenarios show the exact math for 2025. You see gross income drop to taxable levels, and savings add up fast. Let’s walk through four common cases. Compare each to zero deductions for clear wins.

Single Teacher Eases Student Loan Burden

Meet Alex, a teacher earning $55,000. She pays $2,000 in student loan interest. This above-the-line deduction cuts her AGI to $53,000 first. Then she takes the $15,750 standard deduction. Taxable income lands at $37,250.

No deductions? Taxes hit the full $55,000. In the 12% bracket, Alex saves about $2,070. However, her effective rate blends 10-12%, so real savings top $1,800. Check IRS rules on student loan interest to confirm your amount. Simple tracking on loan statements unlocks this.

Married Homeowners Top Standard with Itemizing

Now consider Sarah and Tom, joint filers at $100,000 income. They itemize $8,000 mortgage interest, $20,000 SALT, and $3,000 charity. Total hits $31,000, just edging the $31,500 standard. Taxable income drops to $69,000.

Without deductions, they tax $100,000. At 22% average, savings reach $6,820. High SALT states shine here, thanks to the new $40,000 cap. See TurboTax guide to the SALT changes. Bundle charity next year for even more.

Tipped Server Boosts Take-Home Pay

Jake waits tables, earning $45,000 wages plus $20,000 tips. The new tip deduction covers the full $20,000 above-the-line. After standard $15,750, his taxable income is $9,250.

Zero deductions mean taxing $65,000. In 12%, he pockets $2,400 extra. Service workers stack this with mileage too. Pay stubs prove it easy.

Senior Couple Grabs Bonus Perks

Finally, retired Bob and Ellen file jointly on $80,000 income. They claim $31,500 standard plus $3,200 age add-ons and $6,000 new senior bonus (AGI qualifies). Total deductions: $40,700. Taxable: $39,300.

No breaks? Tax $80,000 at 12-22%, costing $12,000. They save $5,080. Software flags this bonus quick.

Quick Calc: Multiply your marginal bracket by total deductions. Example: 22% x $20,000 = $4,400 saved. Test yours now.

These wins prove deductions work. Run scenarios in TurboTax or ask a pro. You could save thousands this year. Start gathering records today.

Deductions vs Credits: Pick the Best Tax Savers

You know deductions shrink your taxable income. Credits do something different. They slice your final tax bill straight down, dollar for dollar. So which saves more for you? It depends on your bracket and situation. Most people grab both to keep the most cash.

Picture this. A $1,000 deduction in the 12% bracket saves you $120. However, that same $1,000 credit knocks off the full $1,000. Credits pack more punch overall. Deductions shine brighter if you hit higher rates, like 32%, where $1,000 saves $320. Always check both paths.

Here’s a quick side-by-side look:

| Feature | Deductions | Credits |

|---|---|---|

| How it works | Lowers income before tax rates apply | Cuts tax bill after you calculate it |

| Savings example | $1,000 at 12% = $120 saved | $1,000 = $1,000 saved |

| Best for | High earners in top brackets | Anyone; full value no matter bracket |

| Common limit | Phases out at high AGI | Often refundable or non-refundable |

This table shows why you pick based on numbers. Run yours in software for the win.

Grab These Popular Credits Alongside Deductions

Credits come in two flavors: refundable ones pay you back even if taxes hit zero, and non-refundable ones offset what you owe. Families love the child tax credit at $2,200 per kid in 2025. It phases out above certain incomes but stacks easy.

Workers claim the earned income tax credit up to $8,046 for big families. Low earners get the most. Clean vehicle buyers snag up to $7,500 on EVs, though rules tightened. Check IRS credits and deductions page for full lists.

In short, list a few top ones before filing:

- Child tax credit: $2,200 per child.

- Earned income credit: Up to $8,046.

- EV credit: $7,500 for qualifiers.

These add quick wins. Deductions set you up by dropping AGI first.

Maximize Savings: Stack and Avoid Pitfalls

Above-the-line deductions help here too. They lower AGI, so you qualify for more credits without phaseouts. For example, student loan interest cuts AGI and keeps child credit full. Don’t skip them.

A big mistake? Forgetting above-the-line options. People itemize SALT but miss tips or overtime. That bumps AGI and kills credits. Software like TurboTax runs every combo automatically.

Therefore, stack deductions first. Then apply credits. You could double your savings. Test scenarios now. Your wallet thanks you.

Conclusion

Deductions cut your taxable income before rates hit, first through above-the-line options, then standard or itemized paths. For 2025, grab the higher standard deductions, the $40,000 SALT cap, and new breaks for tips up to $25,000 or overtime pay. Stack them like the real-life examples showed, and watch your tax bill shrink.

Therefore, gather your records today. Run the numbers in TurboTax or IRS Free File to pick your best combo. Talk to a CPA if your situation gets tricky, and always double-check IRS.gov because rules shift fast.

Smart moves like these put extra cash back in your pocket for family trips or vacations. What’s your filing deadline? Download our free checklist below to start.