Picture this. You finish a great year freelancing. Then a $10,000 tax bill hits in April. Panic sets in because no boss withheld taxes for you. Freelancers face this often. You pay self-employment tax at 15.3% on net earnings over $400. That covers Social Security and Medicare portions employees split with employers. Plus income tax. If you expect to owe $1,000 or more, make quarterly estimated payments.

Unlike W-2 workers, you handle it all. Good news? A simple system keeps surprises away. You’ll learn steps to calculate, save, and even cut what you owe with deductions. For 2026, single filers get a $16,100 standard deduction. Follow this guide. It makes tax season smooth.

Grasp Your Freelancer Tax Basics to Save Right

Freelancers report income on Schedule C with Form 1040. Add Schedule SE for self-employment tax. Clients send 1099-NEC if you earn $2,000 or more from them. Or 1099-K for $20,000 plus 200 transactions. Track every payment. Because the IRS expects estimates if you owe enough.

Start here to avoid penalties. Self-employment tax funds your future benefits. Employees pay half. You pay full. But you deduct half on your 1040. This lowers income tax a bit. For example, a designer with $50,000 net profit pays about $7,650 in self-employment tax first. Then income tax on the rest.

Pay quarterly to match income flow. Because cash comes unevenly. Set aside from each client payment. This builds the habit now.

Self-Employment Tax Rate and What It Covers

Net business income faces 15.3%. Break it down. 12.4% goes to Social Security up to $168,600 or so. 2.9% funds Medicare with no cap. Singles pay extra 0.9% Medicare over $200,000.

Employees pay 7.65%. Employers match it. You cover both. Yet half your self-employment tax counts as an adjustment. It reduces adjusted gross income. So on $50,000 profit, deduct $3,825. That saves on income tax too.

Most freelancers overlook this full rate. They guess low. Result? Big penalties later. Know it. Plan for it.

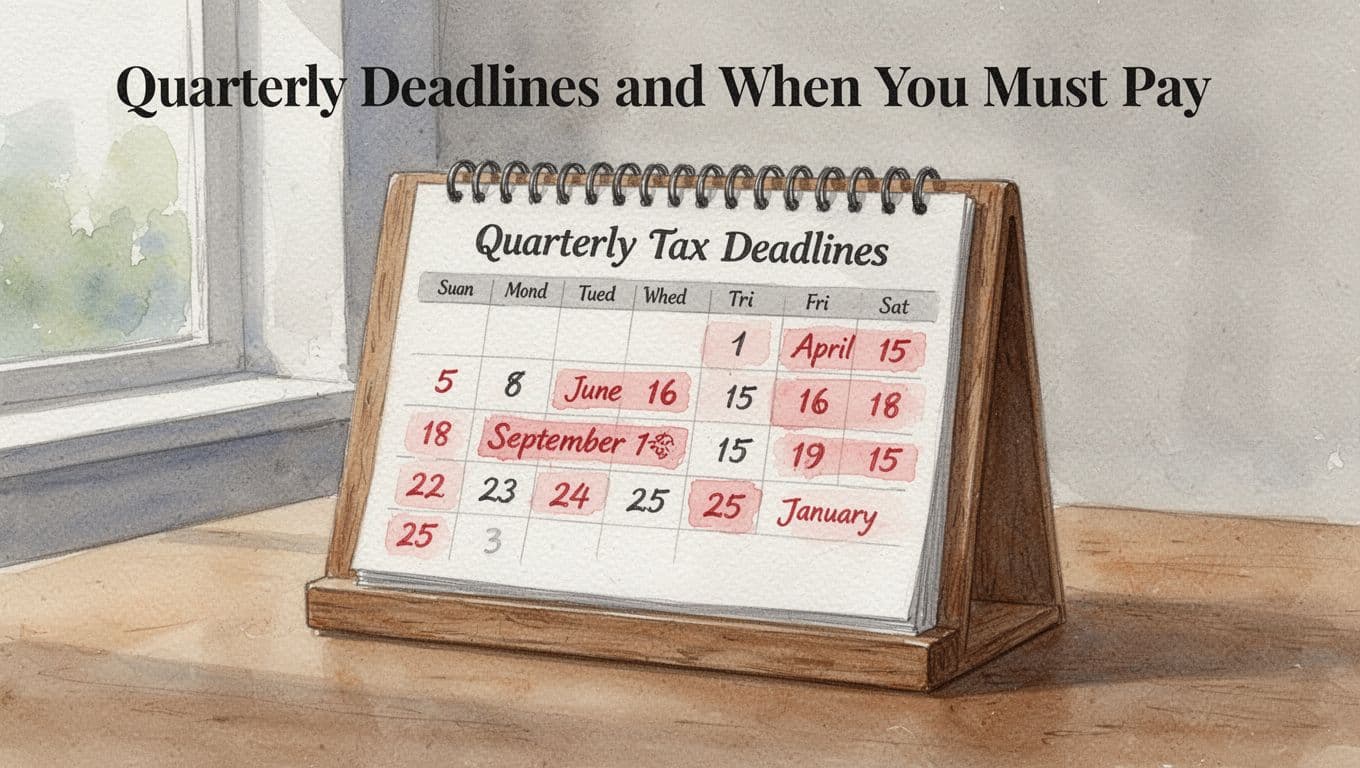

Quarterly Deadlines and When You Must Pay

Mark these 2026 dates. They cover income periods neatly.

- April 15 for January to March

- June 16 for April to May

- September 15 for June to August

- January 15, 2027 for September to December

Owe $1,000 or more? Pay estimates. Skip them, and penalties kick in. They run like interest at 5-8% annualized on the shortfall. Small at first. They add up fast.

Set phone reminders. Because life gets busy. One missed quarter hurts less than all four.

Figure Out Exactly How Much to Set Aside Each Time

Guesswork leads to trouble. Use a safe rule first. Then refine it. Take 25-30% of every invoice. That covers self-employment tax, income tax, and a buffer. Because brackets vary. Deductions change the math too.

For precision, grab the IRS worksheet. It factors your situation. Recalculate if income shifts. Most start simple. Adjust as you go.

A $5,000 monthly earner sets aside $1,250 to $1,500. Spread it monthly. Or quarterly. Either works. The key stays consistent.

Start with the Easy 25-30% Rule

This rule fits most. It handles 15.3% self-employment tax. Plus federal income tax up to 22% bracket for many. State tax adds 5% average. Buffer covers surprises.

A graphic designer earns $80,000 yearly. She saves 28%. That’s $22,400 aside. Deductions drop her net. Still plenty left. He sleeps better. No scramble in April.

Adjust down with big deductions. Up if high income. Test it against last year. Because real numbers guide best.

Get Precise with the IRS Estimation Worksheet

Download Form 1040-ES from the IRS. Fill expected income. Subtract expenses. It spits out quarterly amounts.

Step one: List gross income. Step two: Subtract business costs. Step three: Apply self-employment tax. Step four: Add income tax estimate. Divide by four.

Income jumps mid-year? Redo it. Pay extra then. This keeps penalties away.

Build Habits and Tools That Make Tax Saving Automatic

Systems beat willpower. Open a separate account. Transfer after each payment. Your bank app automates it. No touch needed.

Treat tax money like a client deposit. Untouchable. It grows in high-yield savings. Check top high-yield options for rates over 4%.

Apps track everything. They categorize for Schedule C. Set deadline alerts too.

Open a Dedicated Tax Savings Account

Pick high-yield like Ally or Capital One. They pay interest. No fees. Link your business checking.

After invoice clears, transfer 25-30%. One click. Monthly keeps it easy. Quarterly matches deadlines.

Temptation vanishes. Because it’s not in reach. Interest adds free money. Small win.

Automate Transfers and Use Helpful Apps

Banks offer rules. Set “if deposit over $X, move Y% to savings.” Done.

Try QuickBooks Self-Employed for mileage. FreshBooks for invoices. Wave stays free. See FreshBooks vs Wave vs QuickBooks reviews. They export to IRS forms.

Alerts ping for deadlines. Track expenses real-time. Habits stick fast.

Cut Your Taxes Lower with Freelancer Deductions

Deductions shrink net income. Less tax to save. Half self-employment tax deducts too. QBI gives 20% off qualified income. No phase-out noted for most singles.

New in 2026: No tax on tips or overtime. SALT cap rises for more state tax breaks. Standard deduction hits $16,100 single.

Track with apps. Save receipts. $5,000 expenses on $50,000 income saves $1,500 or more.

Everyday Expenses You Can Deduct Right Now

Home office leads. Use IRS simplified method: $5 per square foot. Up to 300 feet max $1,500.

Measure exclusive space. Deduct portion of rent, utilities, internet. Supplies, software, marketing next. Phone business percent. Pro fees like accountant.

Travel for gigs. Education courses. All count. Start a folder now.

Steer Clear of These Freelancer Tax Traps

Many forget full 15.3% self-employment tax. They save for income only. Shortfall hits hard.

Skip a quarter? Penalties start at 0.5% monthly. Ignore 1099s or records. Lose deductions in audit.

Don’t adjust estimates mid-year. Income doubles? Pay more quarterly. Fix with review habits.

Most traps avoid easy. Use tools. Check quarterly. Complex setup? See a CPA.

Freelancing thrives without tax stress. Habits win.

You now know obligations. Save 25-30% automatically. Deduct smart. Skip traps.

Open that tax account today. Run Form 1040-ES. Chat with a CPA on 2026 rules. Taxes stay manageable. Freelance free.